Ladder is a digital life insurance agency that exclusively offers term life insurance. The company advertises competitive rates, high coverage limits, and happy customers — but is Ladder the real deal?

If you’re thinking about buying life insurance, it can be tough to navigate the marketplace on your own. There are dozens of life insurance providers and multiple types of life insurance to choose from. Plus, there’s the confusing terminology, like ‘death benefit’ and ‘cash value.’

Based on my personal journey as a Millennial life insurance shopper, I’ve concluded that there are a handful of life insurance companies that make the process of purchasing a policy super simple. One of those companies is Ladder.

Check out my experience in this full Ladder review so you can decide if it’s the right fit for you.

Ladder offers addorbable term lengths between 10 and 30 years with a coverage minimum of $100,000 and a maximum of $8 million. The company is unique in that it gives you the option to “ladder” your coverage, which allows you to adjust your death benefit as your family’s financial needs evolve.

- Affordable term life coverage

- Easy application

- Option to “ladder” your coverage

- Only sells term life policies

- No riders available

What is Ladder?

Ladder is a California-based life insurance services provider that was founded in 2015. Since its establishment, Ladder has quickly become an innovator in the insurtech space, earning financial support from reputable investors. The company exclusively offers term life insurance policies, which are issued by third-party carriers.

Pros & Cons

Pros

- Affordable term life coverage — Ladder advertises rates for term life insurance starting at just $5 per month.

- Easy application — You can complete the application online in minutes and get covered on the same day, if approved.

- Option to “ladder” your coverage — Ladder’s signature feature is the ability to “ladder” your term life coverage, which allows you to adjust your coverage limits as your financial needs change.

- High coverage limits — You can purchase a term life policy from Ladder with up to $8 million in coverage, which is sufficient for most young people.

Cons

- Only sells term life policies — The only type of life insurance that Ladder offers is term life insurance. If you want a permanent policy, you need to go elsewhere.

- No riders available — Ladder doesn’t offer any riders for customized protection.

Who issues Ladder’s policies?

Ladder’s term life policies are issued by three licensed life insurance companies — Fidelity Security Life Insurance Company®, Allianz Life Insurance Company of New York, and Ladder Life Insurance Company.

Allianz Life Insurance Company of New York has been rated A+ (Superior) affirmed June 2022 and Fidelity Security Life Insurance Company® has been been rated A (Excellent) based on an analysis of financial position and operating performance, by A.M. Best Company, an independent analyst of the insurance industry. For the latest rating, access www.ambest.com.

These ratings indicate that the companies are financially strong and can meet policyholder obligations and pay claims. In addition, these two companies each have below average customer complaints according to the National Association of Insurance Commissioners (NAIC).

Ladder Life Insurance Company has earned a Financial Stability Rating (FSR) of A (Exceptional) from Demotech, Inc. FSRs are a leading indicator of financial stability, providing an objective baseline of the future solvency. The most current FSRs must be verified by visiting www.demotech.com.

How does Ladder work?

Ladder is aiming to simplify and streamline the life insurance purchase process. And based on my experience with Ladder, it couldn’t be easier to navigate.

When getting a quote, you’ll be asked to provide some personal details, like your age, height, weight, and your tobacco use. I was also asked to disclose my personal and family medical history, my annual income, the number of children I have, and my remaining mortgage balance.

Based on my responses, Ladder’s algorithm estimated how much coverage I would need and for how long. However, I still had the option to choose my own coverage limits and term length.

Ladder’s term life insurance policies are available in term lengths of 10 to 30 years, in 5-year increments, and between $100,000 and $8 million in coverage (up to $3 million in CA). I also learned that the company only offers policies to people between the ages of 20 and 60 years old.

How much does life insurance through Ladder cost?

The cost of life insurance through Ladder depends on a few different factors. For the purposes of this article, I ran quotes with Ladder for two different scenarios, both as a 30-year-old female, and here’s what I got:

- 20-year term, $1M policy: Monthly premium of $34.55/month

- 30-year term, $3M policy: Monthly premium of $147.98/month

I also got quotes from Bestow, one of Ladder’s competitors, to see how its prices stack up. For a 20-year term policy with $1 million in coverage, Bestow quoted me $26.83 per month. For a 30-year term policy, with the maximum coverage limit of $1.5 million, Bestow’s quote was $67.25.

For me personally, Bestow was a cheaper option than Ladder for a 20-year, $1 million policy. However, the cheapest provider is different for everyone. The only way to know how much you’ll personally pay is to get a term life insurance quote from a few different companies and compare them.

Key features

Online application

Ladder’s online application process is really simple. The application is 100% digital, but the company has agents on standby who can answer questions if you need help. When I went through the application process, the entire thing took less than 10 minutes.

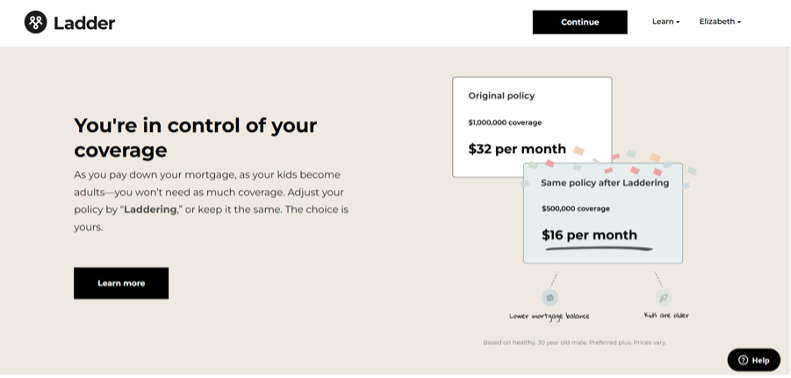

Laddering coverage

With Ladder, you can “ladder up” or “ladder down” your coverage. Essentially, laddering your coverage allows you to adjust your coverage limits — and therefore your monthly premiums — up or down based on how your financial needs change overtime.

For example, you might decide to apply to ladder up if you take on a new mortgage, and ladder down once you’re close to paying that mortgage off. There’s no limit to the number of times you can ladder your coverage, subject to underwriting, and applying is totally free.

Laddering is something that many life insurance companies offer, but they usually offer it through term life riders (add-ons to a regular policy). It’s not an inherent, guaranteed option for most term life policies.

No medical exams (for most people)

If you apply for $3 million in coverage or less, you can skip a medical exam. You’ll just need to answer health-related questions as part of the online application. If you want to get life insurance with no waiting period and no medical exam, it might be worth getting a quote from Ladder.

Riders

One of the biggest downsides of Ladder is that the company doesn’t offer any optional riders that can fill gaps in your coverage. Many other insurance companies offer riders for disability income, critical illness, accidental death, dependent children, etc.

Convertibility

Another negative to Ladder is that you can’t convert a term life insurance policy, because the company doesn’t offer permanent coverage. If you outlive the term, your coverage ends. If you want to keep your coverage in force, you have to purchase a new policy.

Ladder customer service and user reviews

Based on my experience with Ladder, the company seems to have pretty good customer service. You can access an agent via live chat during business hours, which are Monday through Friday, from 8 a.m. to 5 p.m. PT. You can also get in touch with Ladder via phone or email if you prefer.

In addition, Ladder gets few complaints from its customers. Their Ladder’s Trustpilot reviews are mostly positive, which suggests it has good overall customer satisfaction, pricing, and claim processing.

My experience researching Ladder

My experience researching and reviewing Ladder was mostly positive across the board.

The quote and purchase process were very straightforward, and it only took about 10 minutes to complete the application. I also appreciated that Ladder recommended an appropriate term length and death benefit based on my answers. I used the online chat feature to ask a live agent if riders were available (they’re not), and they responded quickly.

Also, Ladder has pretty good reviews from its current customers (based on the Trustpilot reviews I mentioned earlier). That’s not the case with some other life insurance companies I looked at. Ultimately, I would feel confident purchasing a policy from this company, even though it’s not the oldest or most reputable provider on the market.

Who Should Apply for a Policy Through Ladder?

Ladder is a good option if you’re looking for a term life policy with high coverage limits. I would also recommend it to people who want the flexibility of adjusting their life insurance coverage as their family’s financial needs change. Laddering your life insurance is not an option that every life insurance company offers.

Although Ladder didn’t provide the lowest rates for me personally, the company advertises term life insurance starting at just $5 per month, which is pretty affordable. If you’re on a tight budget, and you don’t need a lot of coverage, Ladder might be a good, affordable choice.

Who Shouldn’t Apply for a Policy Through Ladder?

If you’re looking for a permanent life insurance policy, like whole life, Ladder won’t fit your needs. The only option for coverage is term life insurance. Also, Ladder doesn’t offer any riders, so there are no ways to customize your policy with more tailored protection, except for laddering.

The competition

Here’s how Ladder stacks up against some of the other best life insurance options.

| Ladder | Bestow | Lemonade | |

|---|---|---|---|

| Sample quote (20-year, $1M policy) | $34.55/month | $26.83/month | $32.80/month |

| Coverage limits | $100,000 to $8 million | $50,000 to $1.5 million | $50,000 to $1.5 million |

| Policy types offered | Term life | Term life, homeowners, car, renters, and pet. | Term life, homeowners, car, condo, renters, and pet |

| Riders | None | None | None |

Ladder vs Bestow

Bestow is an online-only term life insurance carrier. Like Ladder and Lemonade, Bestow makes it easy to get term life insurance online, with no medical exam. The company offers term lengths of 10, 15, 20, 25, and 30 years, with coverage limits ranging from $50,000 to $1.5 million.

Bestow offers term life insurance that you can apply for in as little as five minutes through a simple online application process.

Terms range between 10 and 30 years (in 5-year increments) and coverage amounts range from $50,000 to $1.5 million. If approved, you'll pay a set monthly premium that will never change throughout the life of the policy. Rates start around just $11 a month.

- Quick, 100% online application process

- No medical exams or doctor's visits required

- Coverage amounts up to $1.5 million

- 30-day money-back guarantee

- No riders offered on term life insurance policies

- Policies not new renew and would require you to re-apply at end of term if desired

If you want the cheapest term life insurance possible, Bestow could be a good provider to look at first. When I compared quotes from Ladder and Bestow, Bestow gave me a lower quote. It was also cheaper than the quote I received from Lemonade for a 20-year, $1 million policy.

» MORE: Get a quote from Bestow or read our Bestow life insurance review

Ladder vs Lemonade Life Insurance

Lemonade Life Insurance is another digital term life insurance provider with an online application and instant approvals. You can choose term lengths of 10, 15, 20, 25, and 30 years, with $50,000 to $1.5 million in coverage.

Lemonade advertises affordable term life coverage, with rates starting at $9 per month. In addition to life insurance, the company also sells other insurance products, like pet, car, and renters insurance, so it could be a good option if you are in the market for multiple policies. Bundling one or more additional Lemonade policies together with your term life policy might give you a discount.

Final thoughts

Based on my experience researching and reviewing Ladder, I think it’s a great company to consider if you’re in the market for term life insurance, especially if you want the flexibility to ladder your coverage. However, keep in mind that there are some downsides, like the lack of riders. Plus, Ladder didn’t give me the lowest quote when I compared its rates to several competitors.