With Lemonade Life, you can apply for coverage if you’re between 18 and 60, and find out if you qualify within minutes — no medical exam necessary.

For busy people in good health, life insurance doesn’t get much simpler or better than this.

Life insurance — you know you need it, but you may not have prioritized buying a policy (don’t worry, you’re not the only one).

In addition to being a great way to provide for your dependents and loved ones if the unexpected happens. Since we’re all getting older by the minute, there’s no time like the present to lock in a great rate.

Lemonade is an excellent insurance provider if you want cost-effective insurance, fast. It’s easy to get a quote and apply to purchase coverage online in just a few minutes on a wide variety of insurance products, including car insurance, condo insurance, home insurance, renters insurance, life insurance, and pet insurance.

- Affordable policies

- Online quotes

- Mobile app

- No permanent life insurance

- No live agents

- Not available in all states

What Is Lemonade Life?

Lemonade is already a well-known name in the insurance space, offering homeowners, renters, and pet insurance. Check out more on those in our full Lemonade insurance review.

They’ve also added term life insurance to their wheelhouse. For young people who want inexpensive, effective coverage, a term life policy is the best kind of life insurance you can get. These policies cover you for a specific time or “term,” between 10 to 30 years, in exchange for a monthly premium.

How Does Lemonade Life Work?

Since Lemonade’s term life insurance offering doesn’t require a medical exam, you can fill out the whole application in one sitting. If you qualify for coverage, you’ll get an approval decision within minutes.

Visit Lemonade’s website or mobile app (I used the website) and click on “Check Our Prices” to start the process with Maya, Lemonade’s friendly artificial intelligence “chatbot.”

Step One: Basic Qualifications

First Maya asked me three qualifying questions:

- Was I between 18 and 60 (Lemonade Life’s age range) with no “serious weight issues”?

- Had I been treated for serious health conditions like cancer or heart disease in the past 10 years?

- Had I used hard drugs or marijuana in the past 10 years?

I’m not sure if positive answers to the last two questions would have automatically disqualified me from coverage — that’s a point I wish Lemonade Life was clearer on.

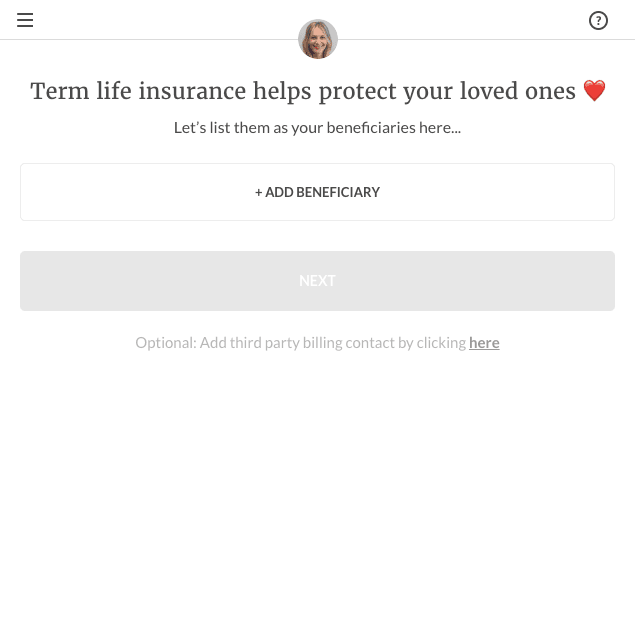

Next, Maya collected my identifying info, then asked me to name one or more beneficiaries — the people who’d receive the death payout if I passed away while my policy was in effect.

You can change your beneficiary down the line if you choose, but it’s a good idea to have someone in mind when you apply.

Maya also asked if I had life insurance coverage elsewhere.

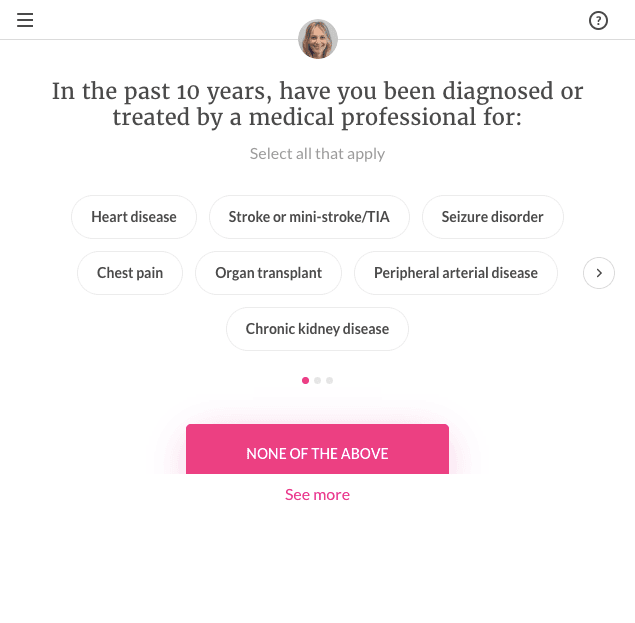

Step Two: Medical History

The next part of the application involves a lot of the health history questions you’d go over with a representative in an in-person medical exam.

These questions ask for details on:

- Tobacco use during the past 12 months

- Medical tests and major diagnoses in the past 12 months

- COVID-19 diagnoses in the past 30 days

- Weight loss in the past six months

- Diagnoses and treatment over the past 10 years for various illnesses

There are two more pages of potential diagnoses after this one, so Lemonade Life is pretty thorough.

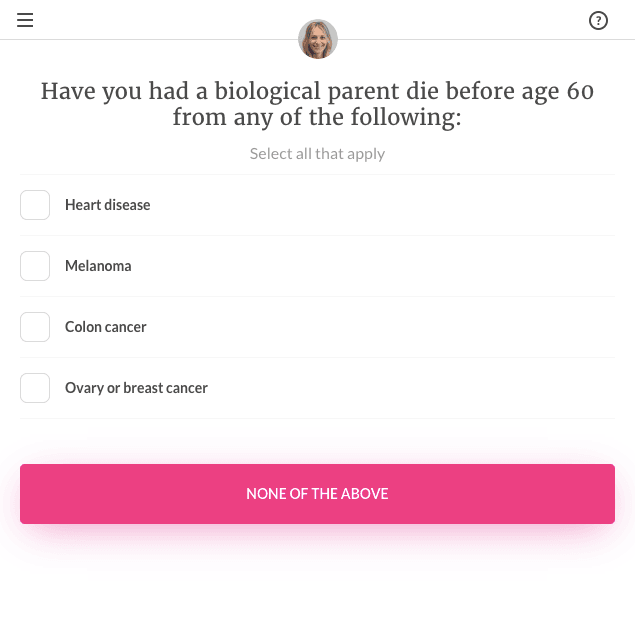

Maya also asks about your family medical history.

Related: How Does Your Health Affect Your Life Insurance Rates?

Step Three: Lifestyle Risk

After some questions about citizenship, residency, employment status, and annual income (you don’t need to provide documents or proof, just check the boxes), Maya moves on to detailed questions about your lifestyle. This is another way the provider measures the risk of insuring you.

Expect questions about:

- High-risk activities (like skydiving, motor vehicle racing, and rock climbing) you plan on in the next two years

- Misdemeanors, felonies, and DWIs in the past 10 years

- Whether you’ve been declined for life insurance in the past two years

- Alcohol and drug use, both current and in the past 10 years

It’s worth noting that when the application asks about marijuana use, they don’t distinguish between recreational and medical marijuana.

Step Four: Application Review

Whew — that seems like a long questionnaire, but the process goes quickly, and I was done in less than five minutes. I “e-signed” with my name and Social Security number, which Lemonade Life requires to prevent fraud. They promise to encrypt this info and keep it confidential.

Finally, Maya reviewed my application, which meant I kept the window open for about five minutes while Lemonade Life’s algorithms worked their accelerated underwriting magic.

Candidates who qualify for a policy select their term length (how long they want coverage) and their preferred coverage amount, then make their first monthly premium payment. Without the need to wait for exam results, it’s an unusually speedy process.

How Much Coverage Does Lemonade Life Offer?

Underwriting is complex, even with Lemonade Life’s accelerated method. At the end of the day, rates will vary based on your age, health, gender, and location, as well as the coverage amount and term you want.

Policies start at $9/month or $108/year. Young candidates in good health who pick low coverage limits might score this rate, but most people will pay higher premiums, especially if they want longer-term lengths (a 30-year policy will cost more than a 10-year policy).

A $20/month or $240/year premium is a more typical range. That’s still lower than the industry average of $359.78/year, making Lemonade’s term life offering an affordable option even if you don’t qualify for rock-bottom rates.

As with all life insurance policies, smokers and tobacco users pay significantly more than nonsmokers.

Lemonade Life Features

Term Lengths

With term life insurance offered by Lemonade, you pick a “term” or time period during which you want active coverage. Choose between 10-, 15-, 20-, 25-, and 30-year terms.

The terms aren’t renewable — once the term runs out, you’ll need to reapply if you want coverage to continue.

But your price remains the same for the length of the term, which is great for future financial planning. Especially if you snag a low rate when you’re young, Lemonade’s consistent premiums can really save you money, since the price won’t change if your health declines or when you inevitably get older.

Coverage Amounts

Lemonade Life – this is one of the things that truly sets them apart – offering Term Life Insurance up to $1.5 million. This amount, also known as the death benefit, is the tax-free total your beneficiaries will get if you pass away during the term.

I was impressed by the range of coverage amounts; no-exam policies tend to have lower coverage limits, and a $1.5 million maximum for no-exam Term life insurance is uncommon.

No Medical Exam

Candidates don’t have to wait for the results of a medical exam to find out if they’ll qualify for coverage. They don’t even have to upload any documents or send in a blood sample.

Lemonade Life keeps things simple by asking all the essential health and lifestyle questions online. That doesn’t mean Maya won’t double-check your info. The electronic application review cross-checked the answers I provided against medical prescription databases and public data sources (like motor vehicle records).

Death Benefit Payout

You have lots of flexibility in choosing a beneficiary for the death payout. You can choose who would be financially affected if you passed away — a family member, a domestic partner, or a business partner. If you name multiple beneficiaries, you’re able to split the benefit between them however you see fit.

The death benefit amount you’ve chosen will go to your beneficiaries tax-free, within a few weeks of their filing a claim. Lemonade Life provides an online form to keep the claim process easy.

Coverage Exclusions

Policies for Lemonade’s term life insurance offering have two major exclusions (circumstances in which they won’t cover a claim):

- If the policyholder provides inaccurate information on their intake form

- If the policyholder dies by suicide within the policy’s first two years

Customer Service

If you have questions Maya the chatbot can’t answer, it’s easy to get in touch with a human Lemonade representative.

- Send a message via the “Help” button (on the website, it’s in the bottom right-hand corner of the screen)

- Email (help@lemonade.com)

- Phone (1-844-733-8666)

- Lemonade’s social media

Cancellation

There’s no charge to cancel a policy, and if you cancel within the first 30 days, you’ll get your first monthly premium refunded in full.

My Experience With Lemonade Life

I’d heard about the convenience of accelerated underwriting methods for life insurance, and it’s true they don’t waste any time.

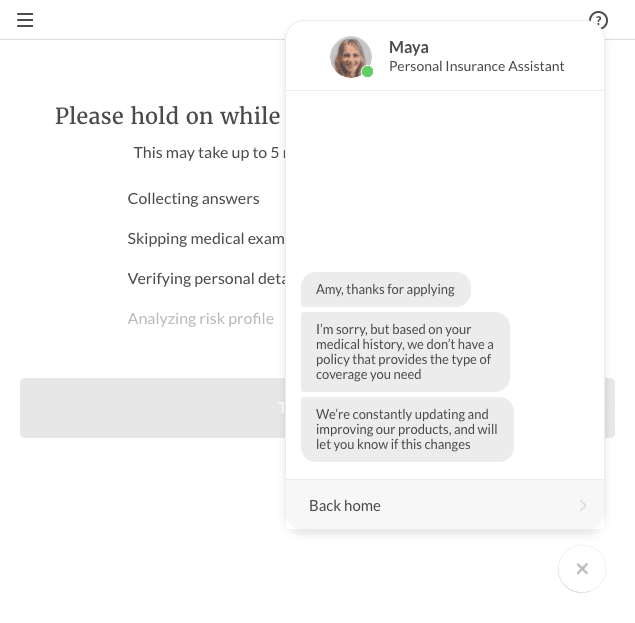

Maya gave me an instant denial so I didn’t have to wait and wonder whether I’d be approved.

Lemonade followed up immediately with an email and attached message explaining why they were declining coverage. The attachment was password-protected — I had to enter my SSN and birth date — which indicates they’re serious about keeping applicant info confidential.

I’d like to see more extensive coverage options for people with various medical conditions. Some providers that issue no-exam policies give you the option of applying for an exam-based policy instead.

Since a detailed medical screening reduces the risk for the insurer (because they have more info about you), the exam can sometimes qualify you for coverage when you’d otherwise be declined, or reduce your rates. Lemonade Life doesn’t offer this option.

But I’d still recommend Lemonade Life for its competitive prices, and it’s absolutely worth filling out the application to see if you’ll get a quote — the process was fast, simple, and completely free!

Who Is Lemonade Life Best For?

Generally Healthy People

Candidates in good health will find it easier to qualify, and they’ll often be able to lock in lower rates, if approved.

People Shopping for Term Life Insurance

For most young people, term life insurance is the easiest, most cost-friendly option to help protect your family’s future.

People Looking for Medium to Large Coverage Amounts

Lemonade Life offers substantial coverage starting at $50,000 and up to $1.5 million, even more than you’ll probably need.

Who Shouldn’t Use Lemonade Life?

People Looking for Permanent Life Insurance

If you want a permanent policy that lasts your entire life and builds cash value, such as whole or variable life insurance, you’ll need to apply with another carrier.

People With Serious Chronic Health Conditions

A history of major medical issues, like cancer, heart disease, and other life-threatening conditions (including some forms of substance abuse) will make it harder to qualify.

New York State Residents

Lemonade Life is available in every state but New York.

Pros & cons

Pros

- Many term options — You have five term options to choose from, which is more than some providers offer.

- High coverage amounts — If you qualify, you can opt for a hefty death benefit up to $1.5 million.

- Easy no-exam application — You can speed through the application process in a few minutes, no tests required.

- All-around insurer — It’s possible to get homeowners’ (or renters’) and life insurance in the same place.

Cons

- No optional riders — Right now Lemonade doesn’t offer riders, or additional benefits you can use to customize your policy.

- Not eligible for Lemonade Giveback — Lemonade’s Giveback program, where they donate unclaimed premiums to a charity, isn’t available with life insurance.

The competition

| Lemonade | Bestow | Fabric by Gerber Life | |

|---|---|---|---|

| Term lengths | 10-, 15-, 20-, 25-, and 30-year terms | 10-, 15-, 20-, 25-, and 30-year terms | 10, 15, 20, 25, or 30-year terms |

| Coverage limits | $50,000-$1.5M | $50,000-$1.5M | $100,000-$5M |

| Policies offered | Term life | Term life | Term life |

Lemonade Life vs Fabric by Gerber Life

More than just an insurance provider, Fabric by Gerber Life strives to help families get the protection they need plus support them with their big-picture financial goals. With Fabric by Gerber Life, you can get term life insurance, create a free will for yourself, and more.

Fabric by Gerber Life was launched by parents for parents to help set up life insurance you need now that there is another member of your family to think about. Quotes are available after taking a 10-minute questionnaire on a sleek and easy-to-use website.

- Easy-to-complete online

- High coverage

- Sub-standard rates

- Not available nationwide

The Fabric by Gerber Life app features all-in-one financial planning tools that let you organize and manage different money accounts from one dashboard. For example, you can start saving for your child’s education, create an emergency fund, and share finances with your partner from the app.

Life insurance is available for term lengths between 10 and 30 years with a coverage minimum of $100,000 and a maximum of $5 million. Policies offered by Fabric by Gerber Life start at $7.86 per month.

Lemonade Life vs Bestow

![]()

Another strong contender in the no-exam life insurance space, Bestow uses data-driven accelerated underwriting. Instead of taking a physical exam, you’ll answer questions about your health and lifestyle online, getting your qualification status within a few minutes. You are eligible if you are 18-60 years old – and if you’re accepted, Bestow shows you possible rates right away.

Bestow specializes in term life policies and their coverage levels are from $50,000 up to $1.5 million, at reasonable monthly rates that start at $10/month.

Summary

Lemonade Life is worth a closer look if you’re in the market for a trustworthy term life insurance policy.

Applying for coverage might be the easiest thing you do all day, and if you’re accepted, you’ll probably lock in a rate that will save you lots of money down the line.