Our simple mortgage calculator will show your total estimated monthly mortgage payment based on:

- The value of the home you’re considering.

- Your down payment amount.

- The interest rate.

- The term (length in years) of the loan.

Learn more how to estimate each variable below or read our beginner’s guide to mortgage loans.

Mortgage Research Center is the Internet's leading source for mortgage rates from dozens of lenders.

Answer a few questions to see your personalized mortgage rates in minutes.

- Purchase or refi

- Won't affect your credit

- Options for first-time buyers, VA and FHA loans

- Must provide your email address

How to use the mortgage calculator

Here’s a breakdown of each field in our simple mortgage calculator.

Note that you only have to enter the first four fields — the rest are calculated for you!

Home value

The home value is the final selling price of the home you’re looking to buy.

Now, you can always just enter the current listing price of the home (i.e., the price you see on Zillow) to get some rough estimates.

But if you want to get even more precise, consider that the average home now sells for around 3% over its listing price, according to Redfin.

So, in order to enter the most realistic number in this field, take the listing price and multiply it by 1.03.

Down payment

Traditionally, a down payment is 20% of a home’s sale price. That’s because 20% is the minimum down payment to avoid having to pay for private mortgage insurance, which we’ll talk about in a bit.

But now that the average home price is nearly $350,000, most folks don’t have $70,000 cash lying around. So the average down payment for first-time homebuyers is now 6%. Depending on your loan type, some lenders will even go as low as 3%.

So what should you put in this field?

For a quick number, enter the amount of cash you think you’ll be able to put together by the time you purchase a home.

For a more precise number, read our article, “How Much House Can I Afford?” By the end of that piece you’ll have a better idea of how much you can afford, which loan type is best for you, and more.

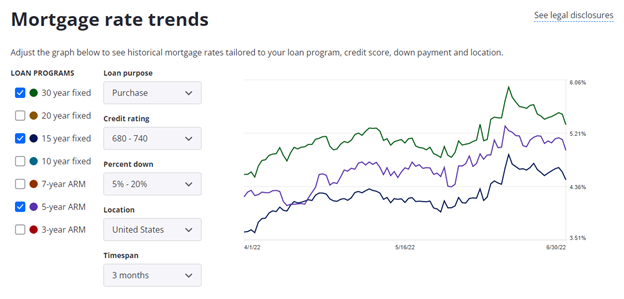

Interest rate

Your interest rate is the one number you won’t want to guess or ballpark.

That’s because a mere 1% difference in your interest rate can change your monthly payment by as much as 10%. So you don’t want to guess wrong and mistakenly think you can’t (or can) afford a particular house.

I recommend using Zillow’s mortgage rate estimator tool — it’s free and will give you a mostly accurate estimate to enter in this field.

When you’re ready to find a lender, check out our real-time mortgage rate table, updated daily:

Length of loan (years)

The term of your loan is simply the length of your mortgage, measured in years.

The most common term is 30 years, though some folks do 15 years to secure a lower interest rate at the expense of higher monthly payments.

Lastly, it’s worth noting that flexible mortgages are becoming a thing, with terms ranging from 8 to 29 years.

But for the majority of folks, 30 years will do just fine so that’s what we’ll put here.

Loan payment

Now that we’ve covered the four input fields, let’s talk output — starting with the loan payment.

The loan payment is strictly the baseline amount of money you owe your mortgage lender each month. It’s merely the crust of the monthly payment pizza, which includes your:

- Principal (your loan amount divided by your total number of monthly payments).

- Interest (what your lender charges you to borrow the money — expressed as annual percentage rate, or APR).

Your loan payment doesn’t include sauce and toppings like your:

- Private mortgage insurance premium, if applicable.

- Property taxes.

- Home insurance.

- Utilities, etc.

So let’s cover those.

Estimated PMI (0.5%) — Private mortgage insurance

If you make a down payment below 20%, your lender will typically require you to get private mortgage insurance, or PMI.

PMI protects your lender, not you. It helps to pay them back if you stop making payments, which in turn makes you less risky to loan money to in the first place.

The bad news is that PMI typically costs between $30 and $70 per month for every $100,000 borrowed. So if you buy a $400,000 house, you could be paying around $200 in PMI premiums each month on top of your loan payment.

The good news is that once you’ve paid off 20% of your house, you can cancel your PMI. So if you make a 15% down payment, you may only have to make a few monthly payments until you can cancel your PMI policy through your lender.

Oh, and if you’re making a down payment of 20% or more, you can safely subtract this PMI estimate from your Total Payment.

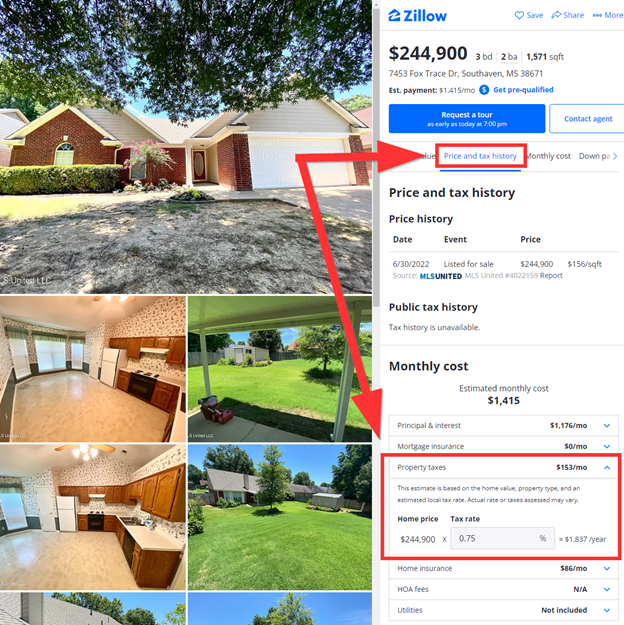

Estimated property taxes

Your property taxes are calculated using the following formula:

Assessed home value x county property tax rate

For a shortcut, you can often find the local tax rate — and the estimated tax payment itself — in the Zillow or Redfin listing. Just head to “Price and Tax History” and scroll down:

One thing to quickly point out is that your future home’s assessed value may be completely different from its appraised value or listing price.

That’s because the assessed value is determined by a tax assessor — a government employee who comes by every few years to estimate the value of the home. Luckily, assessed values tend to be a bit lower than sale prices.

Total payment

Finally, we’ve reached the total payment! This is effectively the total amount you’ll be paying each month to own the home.

Now, while our Simple Mortgage Calculator is perfect for a quick reference, keep in mind that the true number will be coming from your lender. That number might be plus or minus a few percentage points based on market conditions, their fees, etc.

And you’ll also want to factor in homeowners insurance.

Not included: Homeowner’s insurance

Since your homeowners insurance premium isn’t usually considered part of a mortgage payment, we’ve chosen to omit it here.

But it IS an essential cost to owning a home, so let’s briefly talk about it.

Homeowners insurance typically costs between $80 and $150 a month and covers weather damage, home repairs, theft, medical bills if someone else gets hurt on your property, and living expenses if you have to live elsewhere while your place is being fixed up.

How Much Interest Will I Pay on My Mortgage?

How much interest you’ll end up paying depends on which type of mortgage you get: fixed-rate, adjustable (ARM), or interest-only.

Fixed-rate mortgages

As the name implies, a fixed rate mortgage is one where the interest rate is “locked in” and won’t change throughout the course of your mortgage term.

So, if you choose a 30-year, fixed-rate mortgage and your monthly payment comes out to $1,711, guess what? You’ll still be paying $1,711 in 29 years and 11 months, regardless of inflation!

Fixed-rate mortgages are popular because they’re easy to budget around and bring peace of mind that your interest rate won’t ever shoot up.

Adjustable rate mortgages

Adjustable rate mortgages, or ARMs, typically have a fixed rate for the first five, seven, or 10 years — but after that, your interest rate fluctuates based on outside market conditions.

ARMs have lower initial rates than fixed-rate mortgages, but folks still prefer the latter because nobody wants a surprise higher bill in 2028.

That being said, if you know you’ll move out before your intro fixed rate ends, you might opt for an ARM to save a little on interest while you’re in the house.

Interest-only mortgage

Finally, an interest-only mortgage is where you only pay interest — no principal — for the first several years of the loan. And as a form of ARM, they often have an even lower interest rate than fixed-rate mortgages.

Sounds great… so why don’t more folks use them?

For one, they’re pretty hard to get. Lenders only consider borrowers with significant savings, impeccable credit scores, and low debt-to-income ratios for interest-only loans. Second, your monthly payments will skyrocket once your initial interest-only term expires.

Finally, interest-only mortgages aren’t super appealing because you’re not building equity in the home. Until you start paying off the principal, your lender owns 100% of it.

So, why is building equity important?

What’s my home equity

Your home equity is your ownership stake in your home, measured in dollars.

Imagine if you sold your home tomorrow, and used some of the cash to pay off your mortgage with your lender. Whatever’s left over is your equity.

You can calculate your home equity with the following simple equation:

Your home’s fair market value – your remaining mortgage amount

Obviously you won’t sell your home tomorrow, so what’s the point of equity? Bragging rights?

Well, home equity can be used as collateral to get other types of loans. For example, you can get a home equity line of credit (HELOC), which is like a credit card with your home equity set as its credit limit.

And who knows? You might want to sell your house one day and get another one, in which case your old home’s equity is a real dollar amount you can include in your budget for a new home.

Now, before wrapping up a chat about equity, let’s briefly talk about amortization.

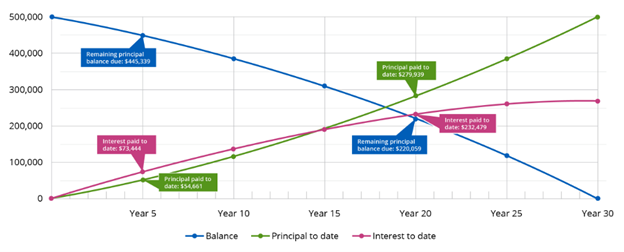

Amortization

Now, it’s important to know that you don’t build equity in a linear fashion. In fact, most of your early mortgage payments will go to paying off your interest, not your principal.

Let’s say you have a $2,000 monthly payment. On paper, $1,500 goes to principal and $500 goes to interest.

But that’s just an average over the course of the loan.

In reality, your lender might apply $1,700 to your interest and $300 to your principal. Next year it’ll be $1,600 and $400, and by year 23 the vast majority of your payment will go to your principal.