Does your debit card have a daily spending limit?

Debit cards have daily spending limits and ATM withdrawal limits that vary by bank and account. Find yours and how to increase your debit card limits.

Debit cards have daily spending limits and ATM withdrawal limits that vary by bank and account. Find yours and how to increase your debit card limits.

An FHA loan is a home mortgage that is insured by the Federal Housing Administration. FHA loans have lower down payment and credit requirements than conventional mortgages, but they may be considerably more expensive.

Here’s a breakdown of what a mortgage is, how a mortgage works, and the most important things to know before shopping for one.

You can work with a financial advisor even if you’re not rich.

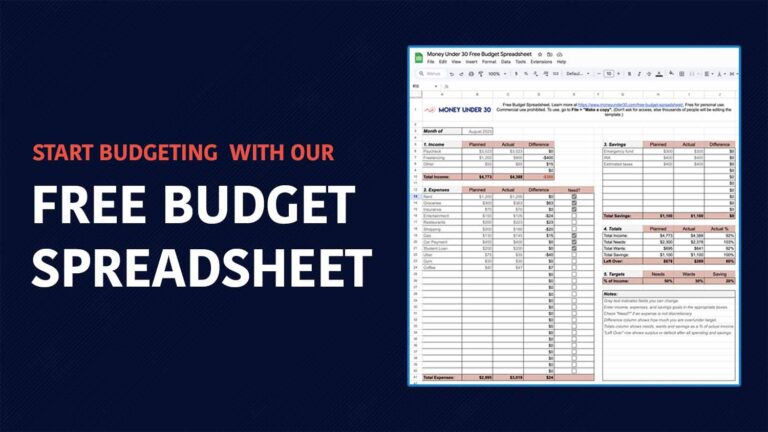

Download our free monthly budget template for Google Sheets or Excel.

Stock analysis provides a crucial foundation for making informed investment decisions. By examining various methods for evaluating a company’s potential for growth and profit, investors can navigate the complexities of the stock market with greater ease.

Establishing clear investment goals is the bedrock of any successful financial strategy. As an individual investor, my primary aim is to create a roadmap that bores through the complexities of the market and aligns my financial activities with my long-term aspirations.

The stock market plays a pivotal role in the global economy. It serves as a barometer for economic health and a platform where companies can access capital by selling shares to the public. For individual investors, the stock market offers an opportunity to own a portion of a company and potentially benefit from its profits and growth over time.

Investing can be one of the most reliable ways to not only preserve wealth but grow it over time. As such, selecting the right strategy is crucial for aligning your investments with your personal goals and risk tolerances.