Investing early is one of the best things you can do for your financial future. And you don’t even need much money to do it.

Many helpful apps, like Acorns, will let you invest just a few dollars at a time, and they can even be linked to your debit or credit card and round up your purchases, investing the difference for you.

Spare change investing apps make investing accessible to everyone by removing the account minimums required by some of the best robo-advisors. But you’ll want to take the fees charged by spare change apps into account when deciding which investment platform is best for your needs.

Here are some of the pros and cons of using micro-investment spare change apps to save money.

Pros of spare change investment apps

The simplicity and low thresholds for spare change investment apps is where they really shine.

Low minimum deposit

Since there’s already a notion that you need a ton of money to start investing, money-saving apps like Acorns and Stash debunk that myth easily. With Acorns, there’s no minimum to open an account and you can start investing with just $5; with Stash, you can start investing with just $0.01.

With these apps, you can easily cut out your morning coffee (or other costly, unneeded daily expenses) for a few days and round-up the money from your other necessary purchases to start investing.

Low fees

Another benefit of these style of micro-investing apps is that there are typically low fees.

Acorns charges $3 a month for its basic Acorns Personal investment plan, with $5 or $9 per month tier options for additional features. These all include real-time round-ups, however, so you may be happy with just the basic tier plan. That would clock in at $36 over the calendar year.

They’re simple to use

Apps themselves tend to be user-friendly and these spare change investment apps are no exception. You can set up your account in minutes and track the progress of your investments and review your options.

Once you set up your account, you won’t have to worry about picking and trading stocks. The money you invest will be placed into a portfolio of Exchange Traded Funds (ETFs) based on the level of risk you choose.

It’s easy to see your earnings, and some apps can even project your earnings years down the road if you continue to make monthly contributions.

Another huge benefit with apps like Acorns and Stash is that they are automatic. You can set up recurring transfers to your account and invest without even thinking about it.

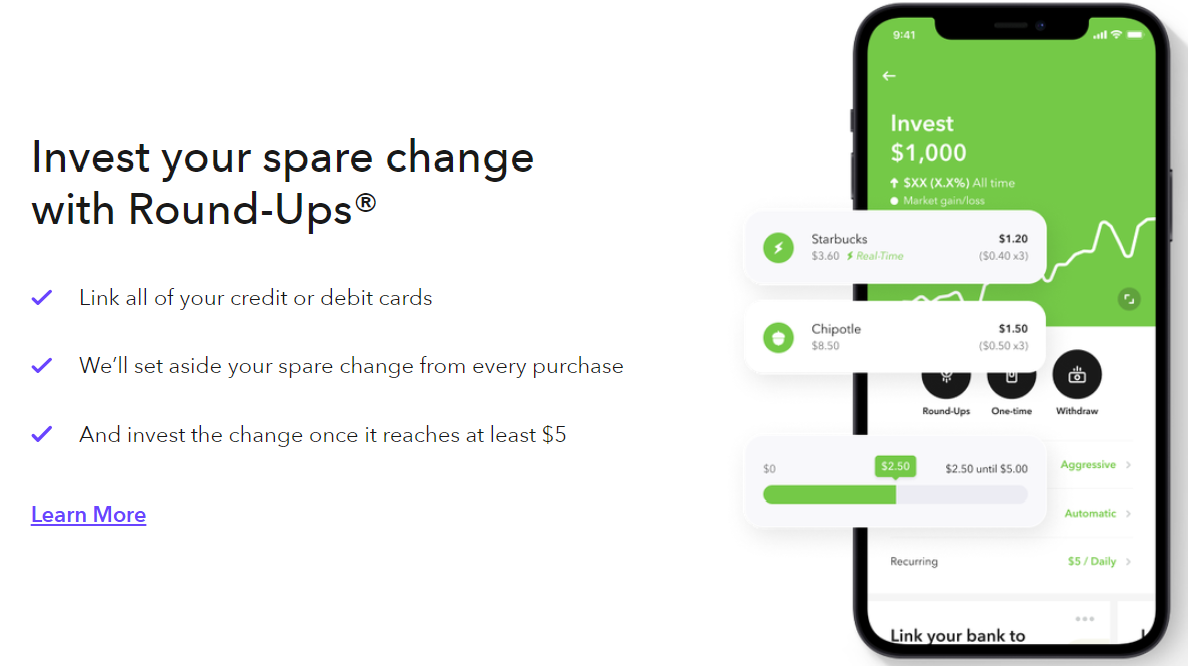

Acorns allows you to invest spare change using their ‘Round-Ups’ system which rounds up all the purchases you make on your linked credit or debit cards to the nearest dollar. That amount is then invested once the change accumulates to a total of at least $5.

Acorns makes it easy to start investing (even if you know nothing) and provides helpful tools to help you save more automatically. In under 3 minutes, start investing spare change, saving for retirement, earning more, spending smarter, and more.

- Effortless automated investing

- Easy-to-use savings features

- Low-cost solution to manage money

- Flat monthly fee more expensive for smaller accounts

- Can use more robo-advisor features

It’s worth noting that Acorns offers ESG (Environmental, Social, and Governance) portfolios. With these, Acorns lets you add socially-responsible companies to your portfolio. You’ll be able to build your portfolio with sustainability in mind.

Stash also allows you to invest in companies that support causes you’re interested in like green energy, tech, and more. What’s better, it only takes a second to choose because Stash does all the research and categorizing for you.

» MORE: Sign up for Acorns or read our full Acorns review

Cons of spare change investment apps

Spare change investment apps aren’t necessarily for anyone, like those who want trade the best stocks right away with the aid of a top brokerage account or hold an exceedingly high balance.

You may invest too little

The idea of investing spare change sounds easy and effective, but you also have to consider your personal goals for investing. If you use an app like Acorns and round up $0.30 of spare change for 60 transactions for the month, you’ve only invested about $15 when you take into account a basic monthly fee.

In other words, while your fee is small, it’s taking up a chunk percentage-wise of what you contributed for the month.

If you can afford to invest $100/month for example (or more would be great), why not set up a recurring transfer for that amount instead? Especially if you’re looking to retire on your investments one day.

Note that while we list this as a con for spare change investment apps that Acorns specifically does solve for this with Smart Deposit. After setting Smart Deposit up, you can have a portion of your paycheck or other regularly-scheduled deposits automatically deposited in your investment or retirement accounts.

Not designed for large investments

These apps aren’t really designed to hold exceedingly large investments. You can find better fees or no fees at all elsewhere with more typical investment accounts if you aren’t limited in terms of how much you can invest.

Limited account options

Some spare change investment apps tend to only offer one type of taxable account to investors, without the option to enroll in a tax-deferred account like a Roth IRA.

This can limit your options if you have specific long-term investment goals, so be sure to compare options properly with what account type you’re looking for.

Acorns does offer Acorns Later feature, designed to help you invest in plans like Roth IRAs.

Who should use a spare change investment app?

Spare change investment apps, like Acorns, can provide a comfortable start and continuing routine to investing for beginners and casual investors. Those struggling to make saving and investing a habit, like millennials, can benefit through spare-change round-ups and automatic deposit features.

They’re also for people looking to pay minimal fees to invest and save with low to no minimum requirements.

The bottom line on spare change investment apps

‘Spare change’ investment apps clearly have the potential to be useful for beginner investors or even college students who have a limited income and want to avoid complex processes and services.

However, you must carefully evaluate the pros and cons and to ensure your earnings are not being eaten up or you’re missing out on a better investment opportunity.

These micro-investing apps are not a good choice for people who prefer to invest in individual stocks commission-free, for example.

If you do use spare change investment apps, be sure to include other personal finance products in your overall investment strategy as you grow more comfortable. You’ll find investment accounts like Wealthfront provide the option to start passively investing with as little as $500 while offering a greater number of features.